Co-author-Ms Riya

Licensing in the pharmaceutical industry involves the legal transfer of development, manufacturing, or marketing rights from one party, i.e., the licensor to another, i.e., the licensee, typically in exchange for a combination of upfront payments, development milestones, royalties, and other financial instruments. What makes licensing particularly valuable is its flexibility as Licensing can support both product- and platform-based collaborations, spanning discovery stage assets to post-marketing arrangements.

Pharmaceutical industry’s growing reliance on licensing is visible in pipeline compositions. According to EvaluatePharma (2024), nearly 45% of late-stage pipeline assets among the top 20 global pharmaceutical companies originate from external sources. This reflects a decisive shift in innovation strategy, from vertical integration to modular collaboration. Another dimension in this shift reflects the increasing complexity and cost of drug development that has prompted pharma companies to access external innovation rather than build everything in-house. Licensing also enables faster entry into new therapeutic areas and geographies, allowing firms to mitigate risk while maintaining a competitive edge. As a result, licensing has evolved from a transactional tool into a strategic pillar of portfolio management.

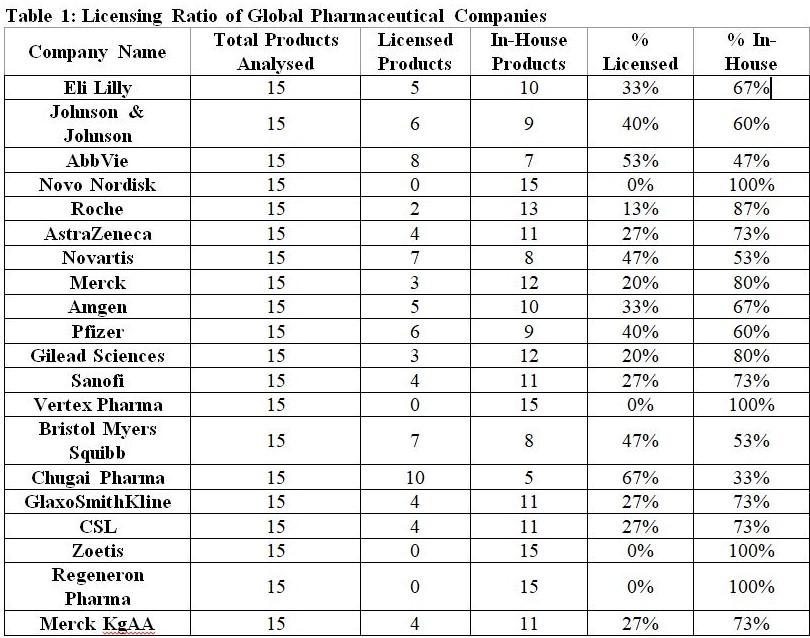

An examination of 40 pharmaceutical (top 20 Global Pharma MNCs and top 20 domestic pharmaceutical companies) present an interesting analysis in this regard. For each company, their top 15 marketed products were evaluated to determine whether they were developed in-house or acquired through licensing. Analysis shows that licensing, once seen as a supplementary tactic, has now become a foundational pillar of many global companies’ innovation strategy. The data given in Table 1 illuminates how deeply embedded in-licensing is across industry leaders and offers a lens into the strategic DNA of the modern pharmaceutical enterprise.

At the high end of the licensing spectrum stands Chugai Pharmaceuticals, with 67% of its portfolio sourced through external licensing. As a part of the Roche Group and a key player in biologics and antibody-based therapies, Chugai’s high licensing intensity reflects its role as a strategic collaborator within global innovation ecosystems. Rather than investing heavily in broad in-house R&D, it leverages partnerships to focus on high-differentiation biologics, often licensed through alliances with academic institutions or biotech startups.

Other major firms with strong externalization strategies include AbbVie (53% of portfolio sourced through external licensing), which relies heavily on in-licensing in areas like immunology and oncology. Deals such as its alliance with Genmab and acquisitions like Pharmacyclics illustrate a conscious pivot toward accessing late-stage, validated assets. Bristol Myers Squibb and Novartis (47% each) demonstrate near parity between in-house and licensed products. Their balanced portfolios suggest a hybrid innovation model where external assets are used to fill gaps, especially in areas like cell therapy, targeted oncology, and RNA-based therapeutics.

Second set of companies is of ‘balanced innovators’ as licensing is not the dominant route followed by these pharmaceutical companies but licensing route plays a complementary role to robust in-house R&D engines. In this group, pharmaceutical companies such as Pfizer (40% in-licensed), Johnson & Johnson (40% in-licensed), Amgen (33% in-licensed), and AstraZeneca (27% in-licensed) reflect a more balanced innovation approach. Pfizer, for example, has historically excelled in forging high-value partnerships, such as its mRNA alliance with BioNTech, while continuing to develop blockbusters like Ibrance and Paxlovid, internally. Its 40% licensing ratio speaks to its open innovation ethos, where agility in deal making complements internal research.

Third category is of those companies which can be termed as ‘In-house Purists’ as these pharmaceutical companies have no externally licensed products in their portfolio (of top 15 marketed products). This holds true for Novo Nordisk, Vertex Pharmaceuticals, Zoetis, and Regeneron Pharmaceuticals, as these companies have reported 0% licensing. This group represents the archetype of the self-reliant, internally-driven innovator, typically characterized by deep domain expertise and platform specialization.

Licensing Ratio of Indian Pharmaceutical Companies presents a fascinating contrast to that of their global counterparts.

While multinational pharmaceutical giants have long embraced licensing as a mainstream innovation strategy, Indian firms have historically adopted a more conservative, inward-looking model of portfolio development. Traditionally anchored in generic manufacturing and process chemistry, Indian companies built their commercial success on in-house capabilities, prioritizing cost-efficiency, regulatory compliance, and large-volume exports over external innovation sourcing.

Out of the 20 top Indian pharmaceutical companies, 13 have reported zero licensed products among their top 15 marketed drugs. Even among firms with some licensing activity, the ratios remain relatively low, only Sun Pharma (47%), Cipla (40%), and Piramal Pharma (33%) show a moderately significant reliance on in-licensing. These figures stand in contrast to global companies like AbbVie (53%), Chugai (67%), or Novartis (47%), where licensing is central to pipeline development.

The low licensing ratios across most Indian firms reflect a long-standing emphasis on in-house development of generics and complex formulations, with innovation centred around ‘reverse-engineering of off-patent molecules’, ‘optimization of manufacturing processes’, ‘regulatory filings in the U.S. (‘Abbreviated New Drug Application’ pathway) and other regulated markets. Companies like Divi’s Laboratories, Lupin, Torrent Pharma, Aurobindo, Glenmark, and Laurus Labs have built global reputations based on technical expertise, not necessarily on external innovation partnerships. Their portfolios remain 100% internally developed, and their product strategies are optimized for operational scale and regulatory efficiency rather than portfolio diversification through licensing.

This model has served Indian pharma well, particularly in building a strong export base in generics and APIs. However, it also implies greater dependence on patent expiries, thin margins, and price-erosion-prone markets, limiting exposure to novel or first-in-class therapies.

Sun Pharma, Cipla, and Dr. Reddy’s Labs appear evolutionary examples. Despite the broader pattern of internal focus, several Indian firms are actively redefining their strategic orientation by incorporating licensing into their business models, particularly in specialty areas where differentiation, innovation, and regulatory complexity create high barriers to entry. Sun Pharma, with a 47% licensing ratio, is the most notable outlier. Over the past decade, Sun Pharma has systematically moved beyond its generic base to build a specialty driven portfolio in dermatology, ophthalmology, and oncology. Key in-licensing agreements of the company include deals with Merck Serono (Ilumya), AstraZeneca, and several smaller biotech firms. Sun’s approach reflects a clear shift toward longer lifecycle products, global presence, and branded portfolios, a strategy that mirrors the licensing-heavy playbooks of many global peers.

Cipla Limited has shown consistent interest in partnering with biotech firms and MNCs to bring novel therapies, particularly in respiratory care, HIV/AIDS, and oncology, to the Indian market. Its 40% licensing ratio suggests a significant reliance on partnerships to enhance therapeutic breadth and maintain first-mover advantage in competitive segments. Dr. Reddy’s Labs (DRL), with a 20% licensing share, is a prominent example of a hybrid strategy, pursuing both biosimilar development and licensing-based access. DRL has actively signed agreements to co-develop or commercialize biosimilars, oncology assets, and complex injectables. Licensing helps DRL accelerate time-to-market in high-growth areas while minimizing clinical development costs and regulatory risk.

Piramal Pharma (33% licensed) and Biocon (13% licensed) represent newer entrants exploring co-development and licensing, particularly in the biosimilars and Contract Development and Manufacturing Organization (CDMO) segments, where collaboration is key to scalability and market access. A critical insight from the Indian dataset is that licensing is used less for innovation and more for access. Indian firms, lacking large-scale discovery pipelines or novel biologics platforms, primarily license products that are already clinically validated, often post Phase-III or even marketed. The rationale is pragmatic as Licensing provides faster entry into regulated markets like the U.S., EU, and Japan. This helps secure exclusive regional rights to differentiated therapies (especially in oncology, biosimilars, or orphan drugs). Licensing enables Indian firms to avoid the high capital intensity and regulatory uncertainty of early-stage R&D.

Unlike global MNCs, which license early-stage or platform technologies to shape the frontier of innovation, Indian pharmaceutical companies license to bridge portfolio gaps, expand product offerings, and capture value in niche high-margin markets. This access-driven strategy has the advantage of cost control and regulatory clarity but limits long-term differentiation unless complemented by internal innovation investments or co-development frameworks. India’s pharmaceutical sector stands at a crossroads, balancing its historical strength in in-house generics with a growing appetite for externally sourced innovation. The current licensing ratios reflect a sector in transition, i.e., while most firms continue to build their portfolios through internal development, a select few are adopting licensing to leapfrog into high-value therapeutic areas and global markets.

As regulatory demands rise and global competition intensifies, licensing is likely to evolve from an optional tool into a strategic necessity for Indian companies aiming to diversify risk, accelerate growth, and elevate their innovation profile on the world stage. Indian pharmaceutical companies have traditionally focused on in-house development, particularly in the generics segment. This approach has been instrumental in establishing India as a global leader in generic medicine production, supplying over 60,000 generic drugs across various therapeutic categories. Pharma companies like Lupin, Torrent Pharma, Aurobindo Pharma, and Glenmark Pharma maintain a 100% in-house portfolio, reflecting a strategic emphasis on cost-effective manufacturing, process optimization, and regulatory compliance. While this model has facilitated significant export growth, it also limits exposure to novel therapies and high margin specialty segments.

Dr. Anil Kumar Angrish-Associate Professor (Finance and Accounting),

Department of Pharmaceutical Management,NIPER S.A.S. Nagar (Mohali), Punjab

Riya- MBA (Pharm.), Department of Pharmaceutical Management,

NIPER S.A.S. Nagar (Mohali), Punjab

Disclaimer: Views are personal and do not represent the views of the Institute.